The End of Fragmented AML Supervision?

What AMLA’s 2025 Roadshow Report Reveals

AMLA’s Roadshow Report is not just a stakeholder engagement exercise. It provides one of the clearest early indicators yet of how the EU’s new Anti-Money Laundering Authority intends to shape supervisory expectations across Europe.

The report highlights recurring concerns around fragmented supervision, uneven AML/CFT maturity across sectors, increasing cross-border financial crime risk, and the growing importance of data and intelligence sharing. For many firms, AMLA will fundamentally change the level of scrutiny applied to AML/CFT frameworks, particularly where governance, data quality and control effectiveness cannot be clearly evidenced.

What is AMLA?

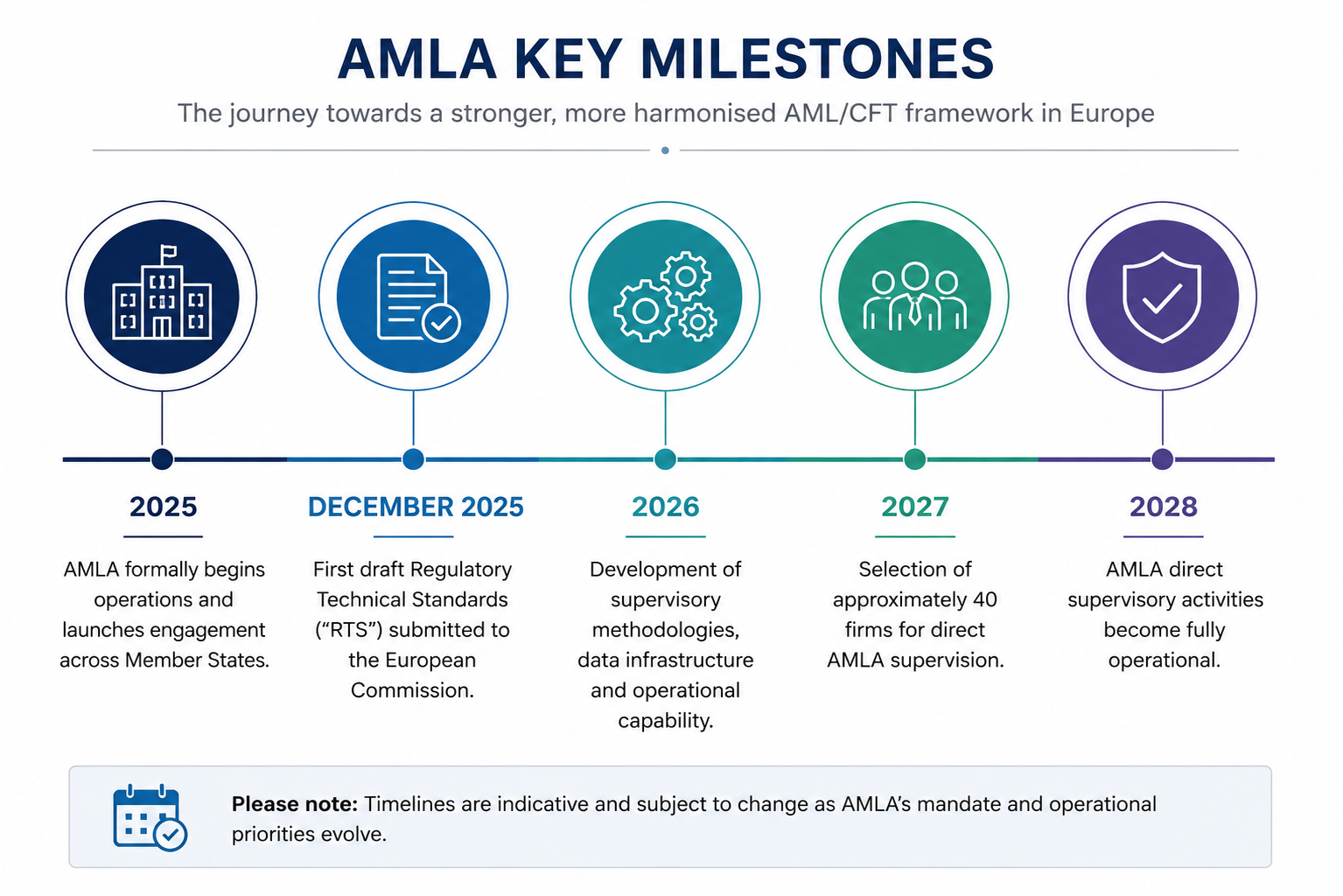

The Anti-Money Laundering Authority (“AMLA”) is the EU’s new central AML/CFT authority, headquartered in Frankfurt and operational from 2025. Its role is to strengthen and harmonise AML/CFT supervision across the EU through the implementation of the new EU AML framework, including the Single Rulebook, while promoting greater consistency between national supervisors and Financial Intelligence Units (“FIUs”).

Although AMLA will directly supervise only a limited number of high-risk cross-border financial institutions, its influence will extend far wider through technical standards, supervisory methodologies, guidance and regulatory expectations adopted across Member States. In practice, AMLA is designed to reduce the long-standing fragmentation and inconsistency that has characterised the EU AML/CFT landscape for years.

The EU Single Rulebook

At the centre of AMLA’s mandate is the EU Single Rulebook.

Historically, AML/CFT requirements were implemented differently across Member States through local transpositions of EU Directives. This often resulted in inconsistent expectations around customer due diligence, governance, reporting and risk management.

The Single Rulebook is intended to create a more harmonised framework through directly applicable EU Regulations and common technical standards. For firms, this means supervisory expectations across jurisdictions are likely to become more aligned, with greater emphasis on consistent group-wide AML/CFT controls and reduced tolerance for localised interpretation gaps.

Key implementation timing

The EU Single Rulebook is expected to apply from July 2027. However, firms should not treat this as a distant implementation deadline.

AMLA is expected to issue a significant volume of Regulatory Technical Standards (“RTS”), guidance and supervisory methodologies throughout 2025 and 2026, which will shape how firms operationalise key AML/CFT obligations in practice.

For many firms, 2026 is likely to become the critical preparation year, particularly for enterprise-wide risk assessments, policy remediation, governance frameworks, data architecture and cross-border control standardisation.

Key themes emerging from the report

1. Fragmentation remains a major concern

A consistent message throughout the report is that firms and stakeholders continue to face significant complexity due to differing supervisory approaches, reporting requirements and interpretations across Member States.

AMLA clearly views supervisory convergence as one of its primary objectives. The message is straightforward: firms should expect increasing standardisation in how AML/CFT obligations are interpreted and assessed across Europe.

For cross-border firms in particular, the ability to justify materially different AML/CFT standards between jurisdictions is likely to diminish over time.

2. Financial crime risks are evolving faster

The report repeatedly references the growing complexity and speed of financial crime risk, particularly in areas such as fraud, crypto-assets, instant payments, online gambling, sanctions evasion and cross-border money flows.

A notable underlying theme is that transaction velocity and digital financial services are reducing the time available for firms to identify and respond to suspicious activity. This places increasing pressure on transaction monitoring effectiveness, real-time risk detection and governance around higher-risk products and channels.

3. AML/CFT maturity remains uneven across sectors

The report is blunt that parts of the non-financial sector lag the financial sector in AML/CFT awareness, resources and capability.

This creates a likely future supervisory focus on DNFBPs, real estate, legal/accountancy services, gambling and other sectors where AML/CFT frameworks, governance structures and control environments have historically evolved less consistently than within mainstream banking and financial services.

This is an important signal. AMLA appears focused not only on improving standards within large financial institutions, but also on raising baseline AML/CFT maturity across the wider obliged entity population.

4. Technology is both a risk and an enabler

The report recognises technology as both increasing financial crime complexity and providing opportunities to improve detection, intelligence sharing and supervisory effectiveness.

AMLA’s focus appears less about prescribing specific technologies and more about improving the infrastructure that supports cross-border AML/CFT cooperation. This includes common reporting standards, stronger data-sharing capabilities and improved intelligence exchange between supervisors and FIUs.

The report also references optimisation of FIU.net, the EU platform used by Financial Intelligence Units to exchange intelligence securely. In practical terms, this points toward faster cross-border information sharing, improved identification of linked suspicious activity and greater expectations around the quality and usability of suspicious activity reporting submitted by firms.

What firms should be doing now

Many firms are still treating AMLA as a future-state regulatory issue. That would be a mistake.

The practical preparation window has already opened, particularly for firms operating across multiple EU jurisdictions or those exposed to higher-risk sectors, products or customer types.

Reassess enterprise-wide financial crime risk assessments

Firms should ensure their enterprise-wide risk assessments are properly evidenced, methodologically consistent and capable of demonstrating clear links between inherent risk, control effectiveness and residual risk outcomes.

AMLA’s direction of travel points firmly toward more data-driven and comparable supervisory assessments.

Review policies and procedures through a convergence lens

Policies built around heavily localised interpretations of AML/CFT obligations may become increasingly difficult to defend.

Cross-border firms should begin identifying unnecessary divergence between jurisdictions and assess whether differences are genuinely required by law or simply legacy practice.

Strengthen governance and management information

Governance frameworks should be capable of evidencing not only that controls exist, but that they operate effectively.

This includes stronger MI around transaction monitoring performance, suspicious activity reporting quality, onboarding exceptions, sanctions controls, overdue reviews and issue remediation.

Prepare for greater supervisory comparability

One of AMLA’s most significant impacts may be the increased ability of supervisors to benchmark firms against one another.

Weaknesses that may previously have remained hidden within local supervisory environments are likely to become more visible in a more centralised and harmonised system.

Final thoughts

The most important point firms should take from the Roadshow Report is that AMLA is not simply harmonising rules, it is harmonising supervisory judgement.

Historically, many firms approached AML/CFT compliance through a jurisdiction-by-jurisdiction lens, shaped largely by local regulatory expectations and market practice.

AMLA changes that dynamic. Increasingly, firms will need to demonstrate that their financial crime frameworks can withstand scrutiny not only locally, but against evolving EU-wide supervisory standards and peer comparisons.

The firms best positioned for this shift will be those that treat AMLA not as a regulatory horizon issue, but as a catalyst for improving governance, data quality, risk assessment methodology and operational resilience across their entire financial crime framework.